How Low Cost Can Chiplets Go? Depends on the Optimization, says AMD’s CEO Dr. Lisa Su

by Dr. Ian Cutress on January 14, 2022 10:00 AM EST- Posted in

- CPUs

- AMD

- APUs

- Trade Shows

- SoCs

- Lisa Su

- Interviews

- CES 2022

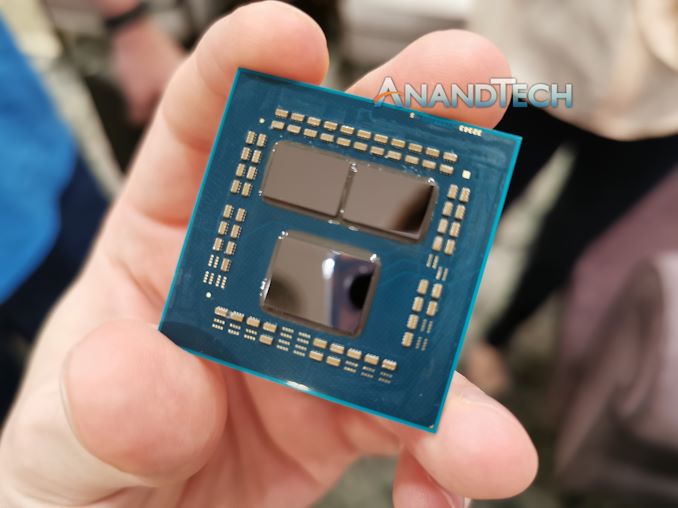

While not the absolute first company in the market to talk about putting different types of silicon inside the same package, AMD’s launch of Ryzen 3000 back in July 2019 was a first in bringing high performance x86 computing through the medium of chiplets. The chiplet paradigm has worked out very well for the company, having high performance cores on optimized TSMC 7nm silicon, while farming the more analog operations to cheaper GlobalFoundries 14nm silicon, and building a high speed interconnect between them. Compared to a monolithic design, AMD ends up using the better process for each feature, smaller chips that afford better yields and binning, and the major cost adder becomes the packaging. But how low cost can these chiplet designs go? I put this question to AMD’s CEO Dr. Lisa Su.

In AMD’s consumer-focused product stack, the only products it ships with chiplets are the high-performance Ryzen 3000 and Ryzen 5000 series processors. These range in price from $199 for the six-core Ryzen 5 3600, up to $799 for the 16-core Ryzen 9 5950X.

Everything else consumer focused is a single piece of silicon, not chiplets. Everything in AMD’s mobile portfolio relies on single pieces of silicon, and they are also migrated into desktop form factors in AMD’s desktop APU strategy. We’re seeing a clear delineation between where chiplets make financial sense, and where they do not. From AMD’s latest generation of processors, the Ryzen 5 5600X is still a $299 cost at retailers.

One of the issues here is that a chiplet design requires additional packaging steps. The silicon from which these processors are made have to sit in a PCB or substrate, and depending on what you want to do with the substrate can influence its cost. Chiplet designs require high speed connections between chiplets, as well as power and communications to the rest of the system. The act of putting the chiplets on a singular substrate also has an effective cost, requiring accuracy - even if 99% accurate placement per chiplet on a substrate means a 3 chiplet product as a 3% yield loss from packaging, raising costs. Beyond this, AMD has to ship its 14nm dies for its products from New York to Asia first, to package them with the TSMC compute dies, before shipping the final product around the world. That might be reduced in future, as AMD is believed to make its next-generation chiplet designs all within Asia.

Ultimately there has to be a tipping point where simply building a monolithic silicon product becomes better for total cost than trying to ship chiplets around and spend lots of money on new packaging techniques. I asked the question to Dr. Lisa Su, acknowledging that AMD doesn’t sell its latest generation below $300, as to whether $300 is the realistic tipping point from the chiplet to the non-chiplet market.

Dr. Su explained how in their product design stages, AMD’s architects look at every possible way of putting chips together. She explained that this means monolithic, chiplet, packaging, process technologies, as the number of potential variables in all of this have direct knock-on effects for supply chain and cost and availability, as well as the end performance of the product. Dr. Su stated quote succinctly that AMD looks for what is best for performance, power, cost – and what you say on the tipping point may be true. That being said, Dr. Su was keen not to directly say this is the norm, detailing that she would expect in the future that the dynamic might change as silicon costs rise, as this changes that optimization point. But it was clear in our discussions that AMD is always looking at the variables, with Dr. Su ending on a happy note that at the right time, you’ll see chiplets at the lower end of the market.

Personally, I think it’s quite telling that the market is very malleable to chiplets right now in the $300+ ecosystem. TSMC D0 yields of N7 (and N5) are reportedly some of the industry best, which means that AMD’s mobile processors in the ~200 sq mm range can roll off the production line and cater for everything up to that $300 value (and perhaps some beyond). Going bigger brings in die size yield constraints, where chiplets make sense. We’re now in at a stage where if Moore’s Law continues, how much compute can we fit in that 200 sq mm sized silicon, and which markets can benefit from it – or are we going to get to a point where so many more features are added that silicon sizes would increase, necessarily pushing everything down the chiplet route. As part of the discussion, Dr. Su mentioned economies of scale when it comes to packaging, so it will be interesting to see how this dynamic shakes out. But for now it seems, AMD’s way to address the sub-$300 market is going to be with either last generation hardware, or monolithic silicon.

This article was updated to clear up some of the language around certainty and conjecture based on rumor.

55 Comments

View All Comments

ikjadoon - Friday, January 14, 2022 - link

Dr. Su's answer here is disappointing after failing to address this for so long: it is rather sad to see Zen3 CPUs stuck at a $300 minimum for 13+ months now. That is far too expensive for most of the OEM market (not to mention budget DIY). The cheapest Zen3 APU with a public price (the 5600G) at $260 is a poor replacement for a full-stack SKU portfolio.AMD has ways to make a profit on lower-end CPUs, too. Ceding the entire low-end to Intel was simply not good for competition nor the consumer in the long-term and AMD will pay for that, unfortunately, with Alder Lake's comprehensive line-up releasing almost a full year before Zen4. A smaller Zen3 CCX (e.g., why not a 6C die to bin to 6C or 4C) would've gone a long way, IMHO. Or significantly expanding their APU availability & reducing their multi-quarter delays,

Of all of Intel's failures and flops, they've always been mindful of the $80 to $200 CPU price bracket because 1) it moves massive volume and market share, ensuring significant market control, 2) gross margins are still quite good, 3) creating an upgrade path within the same generation.

AMD can placate users now that "it's coming", but if Zen4 is anywhere close to Zen3's frankly limiting portfolio, that will be quite a disappointing facet of AMD's revival.

NixZero - Friday, January 14, 2022 - link

retail prices and material cost are linked only when offer competition is so wide to cut down profits.nowaday market is constrained by production capabilities, not competition offer so material cost are not relevant at all, prices are based purely on demand/offer.

Silver5urfer - Friday, January 14, 2022 - link

AMD has many issues due to the sad fate of the x86 market for the past decade before Ryzen, be it the Intel backdoor BS scam forcing them into near bankruptcy or lack of fabs.- First is AMD maximizes highest profit with EPYC as getting marketshare in DC market is very very important. Then Console SoC priorities. Their PC market penetration strategy was peaked with Zen 2, Ryzen 3000. Because of sole reason AM4 vs Intel BS policy of socket EOL despite having proved with a P870DM running a CoffeeLake on Z170. BGA market is also a huge thing for AMD, but they really couldn't manage it well due to Intel literally catering to BGA more than LGA1200 (10nm Tigerlake BGA vs 14nm backport RocketLake disaster)

- Second is TSMC 7N allocation, AMD had to allocate all the above business units it's very tough when the use and throw junk like iPhone A-Series / Smartphone processors get more wafer demand, so they had to cut somewhere, after Zen 3 their marketshare for DIY became HUGE. Which is why AMD did not see the need of drastic price reductions, also on NewEgg 5900X, 5600X were being discounted too after 2021 Q2. Improving availability.

The biggest bummer was Zen3DV refresh. I expected a full stack refresh, but AMD was not interested because of Zen 4 approaching and if Zen3DV gets massive boost and crushes ADL, Zen 4 market adoption would be limited. Plus AM4 is already a lot saturated. Many DIY got AMD only due to AM4 socket longevity. And again the whole EPYC market becomes important. Plus as I said earlier about iPhone and smartphone. Intel and AMD like BGA trash more than anything. Since that is where tons of money is from Client revenue, not DIY. Which is why 6nm Rembrandt was made for BGA rather than a 3DV on 6nm.

AMD is doing pretty strong. Esp no Biglittle trash, Intel made it for BGA market and 10nm limitations. AMD Zen 4 having no such thing, Zen 4 will steamroll over Intel for sure.

The only downsides are - Whole memory being finicky and 12nm IOD having issues even to date with the constant WHEA, USB issues. And the total lack of documentation on the Ryzen chipset and Ryzen CPUs making people to scour over reddit and internet or that horrible discord.

Still no news on what's the node of IOD on Zen 4 Genoa, really curious on which node is that and manufactured where.

plonk420 - Saturday, January 15, 2022 - link

don't skirt around "Intel's BS" ...Intel outright told OEMs like Dell, HP, Gateway, Acer, Fujitsu, Sony, Toshiba, et al to lock AMD out of the market and not make their models AMD (or to minimize use of AMD)lmcd - Saturday, January 15, 2022 - link

This post is a joke right? iPhone retention is high.Zen3DV not getting a full refresh is expected. I was wondering how a two-die Zen3D would work for a while now, and now we know it's more expensive and harder to manage. It also isn't surprising that lower-end SKUs didn't get the cache, that's how Intel's Broadwell caches ended up also (though those were BGA only).

askar - Friday, January 14, 2022 - link

put yourself in AMD shoes. You have 100 sqmm of TSMC N7. Of that you must provide 30 sqmm of capacity to PS5 and XBOX. Then you have the options: $10/mm in profits in datacenter and the demand is for 50 sqmm, $5/mm in desktop Ryzen and demand is 20 sqmm, $3/mm in APUs and demand is 20 sqmm and $2/mm in RADEON and demand is 30 sqmm. What do you do?abufrejoval - Friday, January 14, 2022 - link

They have indeed ceding the entire low-end to the consoles... for which they are producing the proper parts.I guess it would be nice to have those on ITX or in NUCs not only for parts with a broken iGPU, but obviously Microsoft and Sony would take offence (I wonder who's selling the broken parts to the Chinese).

I am pretty sure they have enough chips left to model not only all variations of chiplet combinations but also the profitability for a low-end die variant to satisfy all those who want to play with the red team even on lower-end builds.

And I'm afraid there simply isn't enough of them to aggregate into the type of purchasing power where this becomes profitable with the limited wafer allocations they can obtain.

Targon - Friday, January 14, 2022 - link

What you probably missed is that AMD moved from 4 core per CCX with two CCX per CCD and went to 8 cores per CCD with no CCX. The result is that the lowest target chiplet is 8 cores, with 6 cores there in case there is a failed core. Without making 4-core CCX(or CCD), there is no way to make a quad-core chipset based processor. Volume is how low cost chips end up being even slightly profitable, so high volume of quad-core CCX is how Zen2 was able to pull it off. If/when six core becomes the low end, then sure, chiplet based will be cheap to make due to the high volume of six and eight core CCDs, but AMD will need to get 5 times the number of chips produced before the low end becomes profitable.The monolithic APUs can do the job, but it's not as cheap as doing a TON of CPU dies and GPU dies and then just putting them together would be with high enough volumes. It may be that once Zen4 is out, AMD may do quad-core Zen4 on 7nm for the lower end chiplets, and save the 5nm for the high end of that market.

As far as a limited portfolio, do you really think it makes sense to have 4 different 8 core offerings that are only different due to clock speed differences, or cache size differences? How about making it more confusing where a high cache Ryzen 5 will be faster than a lower cache Ryzen 7? It makes it very clear, how many cores/threads on the chip, and that's it. They all hit the target, no, "this one is 65W TDP, this one is 105W TDP, this one is 80W TDP"...why would you WANT that?

Keep it simple, keep it clear, and be done with it. People just want cheap stuff, without thinking that cheap SHOULD be slower or limited compared to the higher cost stuff. Charging a lot more for only a slight improvement is also unpopular.

dodoei - Friday, January 14, 2022 - link

A digital picture of apes that is processed on these CPUs can sell for 10's of millions. Yet we want to squeeze every penny out of the very cores that make these bubbles possible. Must be sad to be a hardware maker right now.zamroni - Friday, January 14, 2022 - link

That $300 is msrp. Oem buys in bulk and usually gets big discount