Intel Announces Q3 FY 2019 Earnings: Record Results

by Brett Howse on October 24, 2019 11:10 PM EST- Posted in

- CPUs

- Intel

- Financial Results

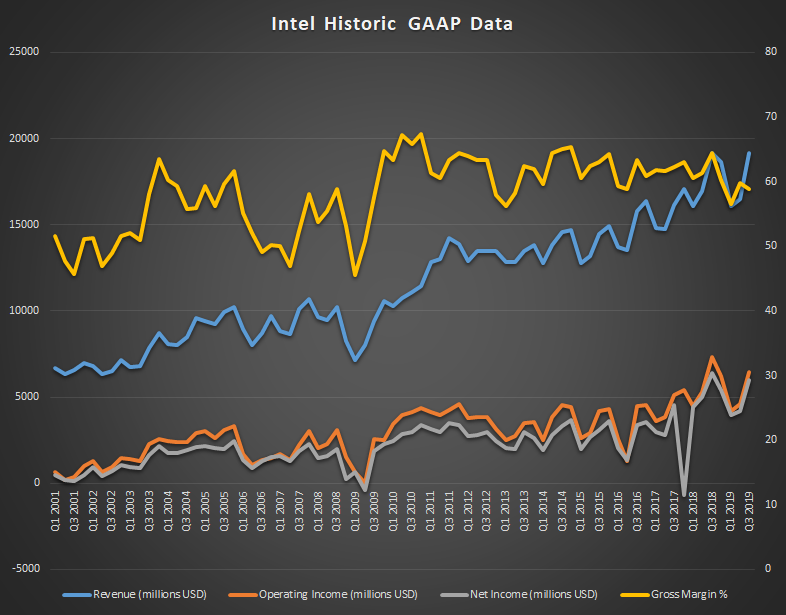

Today Intel announced their earnings for the third quarter of the 2019 fiscal year, which ended September 29, and the company has set a record for revenue thanks to increased growth of their datacenter business. Revenue for the quarter came in at $19.2 billion, beating Q3 2018 by $27 million, which results in a mere 0.14% growth over last year, but enough to make this the highest revenue ever for the company. Gross margin was 58.8%, down from 64.5% a year ago. Operating income was down 12% to $6.4 billion, and net income was down 6% to $6.0 billion. This resulted in earnings-per-share of $1.35, down 2% from a year ago.

| Intel Q3 2019 Financial Results (GAAP) | |||||

| Q3'2019 | Q2'2019 | Q3'2018 | |||

| Revenue | $19.2B | $16.5B | $19.2B | ||

| Operating Income | $6.4B | $4.6B | $7.3B | ||

| Net Income | $6.0B | $4.2B | $6.4B | ||

| Gross Margin | 58.9% | 59.8% | 64.5% | ||

| Client Computing Group Revenue | $9.7B | +10% | -5% | ||

| Data Center Group Revenue | $6.4B | +28% | +4% | ||

| Internet of Things Revenue | $1.0B | +1% | +9% | ||

| Mobileye Revenue | $229M | +14% | +20% | ||

| Non-Volatile Memory Solutions Group | $1.3B | +38% | +19% | ||

| Programmable Solutions Group | $507M | +3.7% | +2% | ||

Intel splits their business into two main areas. The Client Computing Group is the PC-Centric products, and the Data Center Group consists of everything else. Despite the contraction of the PC market over the last several years, it has continued to be the main source of revenue for Intel, and that continues this quarter as well, but only by a small margin. The Client Computing Group revenue was down 5% year-over-year to revenue of $9.7 billion. Intel attributes this drop to lower year-on-year platform volume, although loss was partially offset by some of the higher-cost products especially in the commercial segment.

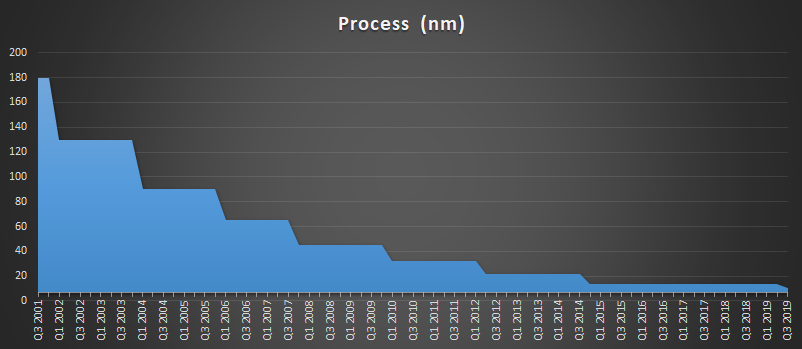

Although the overall PC side from Intel was down, Intel has only just launched their latest 10th generation Core products which won’t make up much of Q3’s numbers due to the cut-off date of the end of September. Intel now has over 30 devices launched based on the 10 nm Ice Lake platform, signalling the end of 14 nm which has been iterated on many times over the last several years as Intel struggled to get their 10 nm process off the ground. The good news for Intel is that despite the initial setbacks for 10 nm, they have stated that 10 nm yields are actually ahead of their internal expectations for this point in its lifecycle, which should help alleviate some of the backlog the company has been facing with production assuming the can use the improved yields to transition more of their lineup over to 10 nm a bit quicker. Intel has also stated that despite the years lost on 10 nm, they are moving back to a 2 to 2.5 year process cadence, with 7 nm on track for their GPU lineup in 2021.

Intel lumps the rest of their business into the “Data-Centric” role, and this side of the company has been making strong gains over the last several years, and now almost matches the Client Computing Group in total revenue at $9.5 billion, versus $9.7 billion for the CCG. But Data-Centric includes not only the Data Center Group, but also Internet of Things, Mobileye, Non-Volatile Storage, and Programable Solutions. Altogether these segments achieved record revenue, up 6% from 2018. Individually, Data Center Group was up 4% to $6.4 billion with a strong mix of Xeon sales and growth in all segments. Internet of Things also had record revenue, up 9% to $1.0 billion. Mobileye is also on the record train, with a 20% year-over-year gain to $229 million, as did Non-Volatile Storage which was up 19% to $1.3 billion. Programable Solutions was the only segment in the Data-Centric listings to not hit a record in revenue, but it was still up 2% to $507 million for the quarter, and they shipped their first 10 nm Agilex FPGA this quarter as well.

Looking ahead to Q4, Intel is expecting revenue around $19.2 billion with earnings-per-share of $1.28.

Source: Intel Investor Relations

39 Comments

View All Comments

Targon - Friday, October 25, 2019 - link

So, Q3 2018 to Q3 2019, Revenues are flat, Operating and Net Income are DOWN, and profits are down. Data Center is ALWAYS on a cycle, you don't think that businesses replace their servers every year, do you?I don't see a lot of good news from this report, no matter that Intel is trying to spin it as good news. Intel is still making big profits, but I expect things will be more interesting when we see the numbers from AMD next week, purely because AMD has been recovering well with their new processor lines. Quarter to quarter...yea, third quarter always has a bump in income due to back to school, and preparation by OEMs for the holiday shopping season and needing to get inventory levels ready. Remember, before any business sells a product, they need to have product in hand. If they don't have product ready to ship 3-4 weeks ahead of Black Friday, they are running a risk of there being a shortage.

yeeeeman - Friday, October 25, 2019 - link

Whatever people say here, the fact that a company stuck on a 5 year+ old process can post such results is showing that they are managing things the right way.I would imagine that making a Core i9 9900K on an ancient process is much cheaper for Intel than what AMD pays for 3700X (one 7nm die and one 12nm). So given the fact that both CPUs sell at the same price, even if Intel sells less units compared to AMD, the end result is that Intel will still make more money.

As for 10nm+ process, I think this time Bob is saying the actual truth. IceLake seems to be quite a good improvement over Whiskey Lake in terms of performance per watt. Don't know about density, but I would expect it to be quite a bit better. This whole 10nm fiasco came from changing lots of stuff (production wise) in one single node. The idea, if it worked, was very good and Intel could have said in 2017 that its 10nm process is as dense as TSMC 7nm.

In any case, any mistake done in the development means you will be delayed. When you screw up the entire process premises, you first have to try to find solutions and that I expect it to be somewhere in 2017, followed by a hard decision to start from scratch from 14nm. This took two more years. I don't think Intel has forgot how to make chips. I think they just made the wrong bets. TSMC, Samsung would have the same delay if they would screw things up, because it takes a lot of time to develop, test, scale with profit a certain process. The fact that we see such a fast cadence from TSMC is just because they have teams working in parallel.

All in all, I think Intel needs to push 7nm as early as possible. They also need to use chiplets like AMD. The fact that they announced Foveros and EMIB last year means that they intend to take this path also. I say we shoudn't jump to conclusions in regards to Intel/AMD since things can change very fast. And given how well Intel managed this whole 10nm situation, I think they have big plans for future once things start to settle on the manufacturing side of things.

stockolicious - Friday, October 25, 2019 - link

" I say we shoudn't jump to conclusions in regards to Intel/AMD since things can change very fast."Things don't change fast - server guys are now jumping ship with Rome - EPYC they used basically just to validate. AMD is doing very well in the DIY market. I Agree INTC needs a chiplet approach and on 7nm but even at that point AMD will be competitive. The difference this time around with AMD is that they have a great MFG partner - in the past they would step on their own feet owning glofo. AMD set itself up to be competitive for the next many years.

WaltC - Friday, October 25, 2019 - link

Not surprising--after AMD's decisions during the A64/Opteron era moved the markets to DDR SDRAM and x86-64 (which AMD licensed to Intel years ago), at a time when Intel was pushing RDRAM and Itanium as "The only 64-bits you'll ever need"....Also, I see Intel's current Q3 report as more evidence of its heavy diversification into money/financial markets combined with the sort of clever accounting "tricks" that all companies use for a quarter or two when things are turning south. Intel cannot survive as a competitive force to AMD without new architectures (although Intel could easily survive as a different kind of company, probably), and we have seen none of that to date. Continuing to milk and heavily discount its old architectures will only buy them so much time. If we had a "performance watt" investment metric concerning how much a given company spends to develop per "performance watt," AMD would come out way ahead on that scale, as they to date have done much more than Intel with far less $$$ spent--so of the two companies in terms of their chips businesses, AMD clearly is the better-managed company today, imo.RSAUser - Wednesday, October 30, 2019 - link

"much cheaper for Intel than what AMD pays for 3700X"No, because AMD uses a chiplet design those 3700X core complexes are the worst of the stack. In the case of AMD's chiplet design, you have to take the entire stack into account to actually understand what the true cost of it is.

Intel's stacking design is also quite interesting, will see how that goes, it's really nice that CPU's have finally been moving forward again, just wish GPU was in the same market rather than Nvidia completely owning it.

WaltC - Friday, October 25, 2019 - link

What I find amusing these days is that while both Intel (now deeply discounting) and AMD show clear signs of their processor/chip businesses growing year over year, some people keep saying that the PC market is contracting. Instead of looking at the bottom line of the companies who make the hardware, they choose to look at various "estimates" like Peddie or even, bizarrely, the 100% voluntary Steam survey (you have to opt-in to the ss, it isn't automatic with a Steamworks account)...;)Intel's main income is overcharging precipitously in the enterprise/server markets. AMD has only just begun to hammer Intel where it hurts in those markets. People accustomed to thinking that AMD will simply fizzle "inevitably" should adjust their thinking to incorporate the concept that AMD today is a different company entirely from what it was during its heyday A64/Opteron era. Today's AMD is far different and is already planning several years ahead. Right now, for Intel, the only way they can keep the revenue from their chips businesses flowing is to discount heavily, as there is little other reason *not* to go AMD these days. This may change when/if Intel is able to market competitive products at competitive prices looking ahead, certainly. AMD's server share will be appropriating ~10% per year of the entire enterprise market, I should think. Should be great fun to watch...;)

WaltC - Friday, October 25, 2019 - link

Wanted to add that AMD's Q3 report is due in four days, Oct. 29--that is going to be interesting!RSAUser - Wednesday, October 30, 2019 - link

I don't think Intel is in a bind, not even close, they have a huge market outside of just pure CPU, and they're changing their design/product strategy to incorporate that.AshlayW - Saturday, October 26, 2019 - link

This probably isn't going to continue if ROME has anything to say. Intel's Xeon brand might as well be irrelevant the way things are going. Which is good for the short/medium term, because a strong AMD means a healthier overal market for everyone. Businesses, consumers and human progress overall.