Intel Announces Q3 FY 2019 Earnings: Record Results

by Brett Howse on October 24, 2019 11:10 PM EST- Posted in

- CPUs

- Intel

- Financial Results

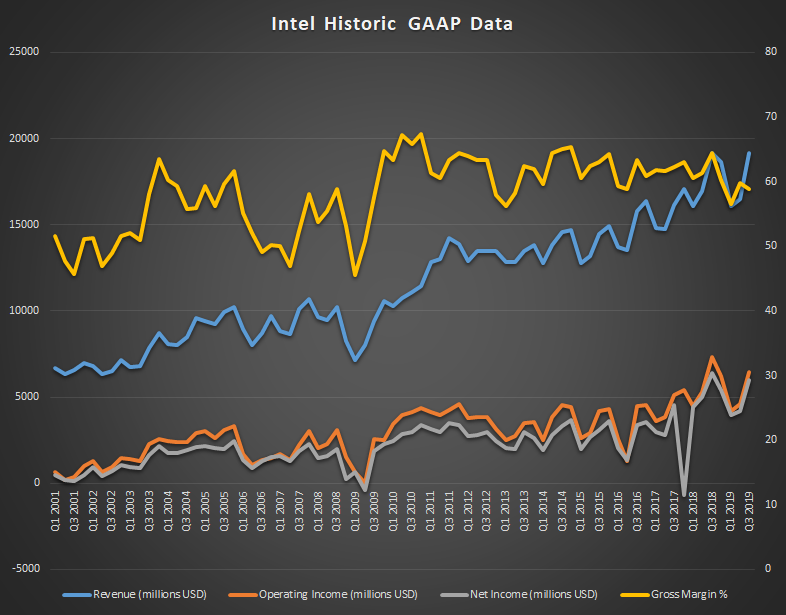

Today Intel announced their earnings for the third quarter of the 2019 fiscal year, which ended September 29, and the company has set a record for revenue thanks to increased growth of their datacenter business. Revenue for the quarter came in at $19.2 billion, beating Q3 2018 by $27 million, which results in a mere 0.14% growth over last year, but enough to make this the highest revenue ever for the company. Gross margin was 58.8%, down from 64.5% a year ago. Operating income was down 12% to $6.4 billion, and net income was down 6% to $6.0 billion. This resulted in earnings-per-share of $1.35, down 2% from a year ago.

| Intel Q3 2019 Financial Results (GAAP) | |||||

| Q3'2019 | Q2'2019 | Q3'2018 | |||

| Revenue | $19.2B | $16.5B | $19.2B | ||

| Operating Income | $6.4B | $4.6B | $7.3B | ||

| Net Income | $6.0B | $4.2B | $6.4B | ||

| Gross Margin | 58.9% | 59.8% | 64.5% | ||

| Client Computing Group Revenue | $9.7B | +10% | -5% | ||

| Data Center Group Revenue | $6.4B | +28% | +4% | ||

| Internet of Things Revenue | $1.0B | +1% | +9% | ||

| Mobileye Revenue | $229M | +14% | +20% | ||

| Non-Volatile Memory Solutions Group | $1.3B | +38% | +19% | ||

| Programmable Solutions Group | $507M | +3.7% | +2% | ||

Intel splits their business into two main areas. The Client Computing Group is the PC-Centric products, and the Data Center Group consists of everything else. Despite the contraction of the PC market over the last several years, it has continued to be the main source of revenue for Intel, and that continues this quarter as well, but only by a small margin. The Client Computing Group revenue was down 5% year-over-year to revenue of $9.7 billion. Intel attributes this drop to lower year-on-year platform volume, although loss was partially offset by some of the higher-cost products especially in the commercial segment.

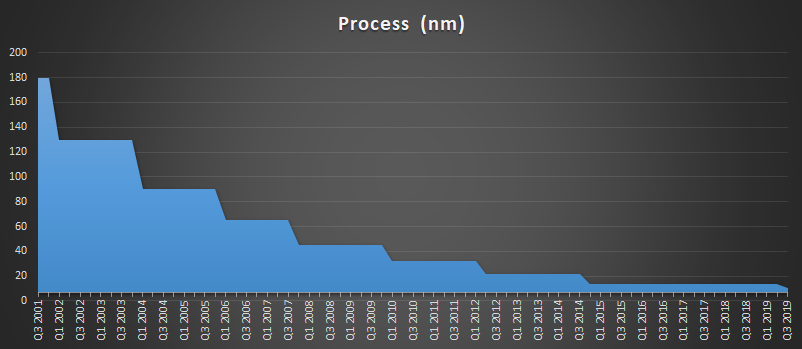

Although the overall PC side from Intel was down, Intel has only just launched their latest 10th generation Core products which won’t make up much of Q3’s numbers due to the cut-off date of the end of September. Intel now has over 30 devices launched based on the 10 nm Ice Lake platform, signalling the end of 14 nm which has been iterated on many times over the last several years as Intel struggled to get their 10 nm process off the ground. The good news for Intel is that despite the initial setbacks for 10 nm, they have stated that 10 nm yields are actually ahead of their internal expectations for this point in its lifecycle, which should help alleviate some of the backlog the company has been facing with production assuming the can use the improved yields to transition more of their lineup over to 10 nm a bit quicker. Intel has also stated that despite the years lost on 10 nm, they are moving back to a 2 to 2.5 year process cadence, with 7 nm on track for their GPU lineup in 2021.

Intel lumps the rest of their business into the “Data-Centric” role, and this side of the company has been making strong gains over the last several years, and now almost matches the Client Computing Group in total revenue at $9.5 billion, versus $9.7 billion for the CCG. But Data-Centric includes not only the Data Center Group, but also Internet of Things, Mobileye, Non-Volatile Storage, and Programable Solutions. Altogether these segments achieved record revenue, up 6% from 2018. Individually, Data Center Group was up 4% to $6.4 billion with a strong mix of Xeon sales and growth in all segments. Internet of Things also had record revenue, up 9% to $1.0 billion. Mobileye is also on the record train, with a 20% year-over-year gain to $229 million, as did Non-Volatile Storage which was up 19% to $1.3 billion. Programable Solutions was the only segment in the Data-Centric listings to not hit a record in revenue, but it was still up 2% to $507 million for the quarter, and they shipped their first 10 nm Agilex FPGA this quarter as well.

Looking ahead to Q4, Intel is expecting revenue around $19.2 billion with earnings-per-share of $1.28.

Source: Intel Investor Relations

39 Comments

View All Comments

Quantumz0d - Friday, October 25, 2019 - link

That's why the name Chipzilla. LOLAnd here we have people who want BGA A series in their machines and Apple mass producing them to feed their cravings of a closed OS and closed ecosystem. While Apple itself is running on Linux for their services.

jlp2097 - Friday, October 25, 2019 - link

Amazing. AMD has arguably better and cheaper products in PC space (not mobile!) and data center space, yet not even a dent in Intels financials. Quite the opposite, they are growing. I don't get it... Really curious about AMD next quarterly financials.klatscho - Friday, October 25, 2019 - link

I would say they have stagnated since last year, because the TAM has grown and revenue stayed roughly the same. Also "Gross margin was 58.8%, down from 64.5% a year ago. Operating income was down 12% to $6.4 billion, and net income was down 6% to $6.0 billion. This resulted in earnings-per-share of $1.35, down 2% from a year ago." Not much, but AMD has made a small dent in their margins and hence profits.jlp2097 - Friday, October 25, 2019 - link

I mostly agree with you, esp. that margins are down somewhat - but by much less than I would have thought. Any source to back up the TAM growth statement? Did I miss something?Targon - Friday, October 25, 2019 - link

Intel has counted on OEMs and kickbacks to keep their position. You don't see nearly as many AMD Ryzen based offerings as there should be. You don't even see the 2019 batch of desktop APUs out there at decent prices(you still see the 2200g, barely any 3200g based desktops, I've not seen even the 3400g in generally low cost desktop machines from OEMs). Finding a big OEM desktop machine with a Ryzen 5 or 7 in it these days isn't common either. The only reason, when the new chips WILL work on previous generation motherboards, would be payments by Intel to keep these OEMs from offering decent AMD based machines.duploxxx - Friday, October 25, 2019 - link

not a dent?Look at Gross Margin?

Dont Forget that EPYC1 was just an intro, EPYC2 will hit Datacenter revenue hard. Not just because they will have reduced market share but they also had to decrease there pricing with 30%.

On top of that they had to create a beast of a SP BGA 9000 platform that nobody wanted in the end in mass production.

To close off in 2020 they are in such a bad shape with the withley platform that they will have to convince OEM and customers that they have 2 platforms in 1.... Cooper lake (a glued multidie) and Whiskey lake ( a failed 10nm platfrom) with different features and capabilities.

THis is just the top of the iceberg, results will be very visible in the at least the next 5-6 quarters.

And dispite the fact that this is not good, it actually is, because remember as a customer it is good to have competition and to see companies have a drawback, when they believe they are invincible .Pricedrops - improved features and tech - higher investments back into the product.... in stead of just increasing margins.

Kishoreshack - Friday, October 25, 2019 - link

It will take time to show upthe AMD products were launched recently

it will take time to affect intels earnings

AshlayW - Saturday, October 26, 2019 - link

Consumer stupidity/Mindshare takes many years to erode.brakdoo - Friday, October 25, 2019 - link

"The good news for Intel is that despite the initial setbacks for 10 nm, they have stated that 10 nm yields are actually ahead of their internal expectations"LOL, Bob Swan said the same during the q2 earnings release:

"Both yield and defect density are ahead of schedule for our 10-nanometer data center products."

Even in Q1 Bob said:

"And that played out as we expected, because I mentioned in my prepared remarks that our progress and our improvement on 10-nanometer yields was in line with what we've expected coming into the year, a little bit better, "

Brett, you should scale back your expectations that there was a sudden change and 10 nm is fine now.

Targon - Friday, October 25, 2019 - link

Hasn't Intel been saying that 10nm is on track since the end of 2015? Why would anyone believe ANYTHING from Intel at this point? Why Intel didn't get a big fine for what is obviously false reporting for at least three years is obviously kickbacks and bribes. If you lie to your investors, that SHOULD result in penalties.